Roth IRA — Explained

Apr 15, 2025

🔥 Here’s a truth bomb:

🖥️ Reading time: 3 minutes

“If you’re not using a Roth IRA, you’re voluntarily signing up to pay more taxes—forever.”

Most people think retirement planning is just about stashing money away. But if you’re not thinking about how your money gets taxed later, you’re missing the point. That’s where the Roth IRA comes in. It's not just another account—it's a tax strategy disguised as a savings tool.

Let me break it down:

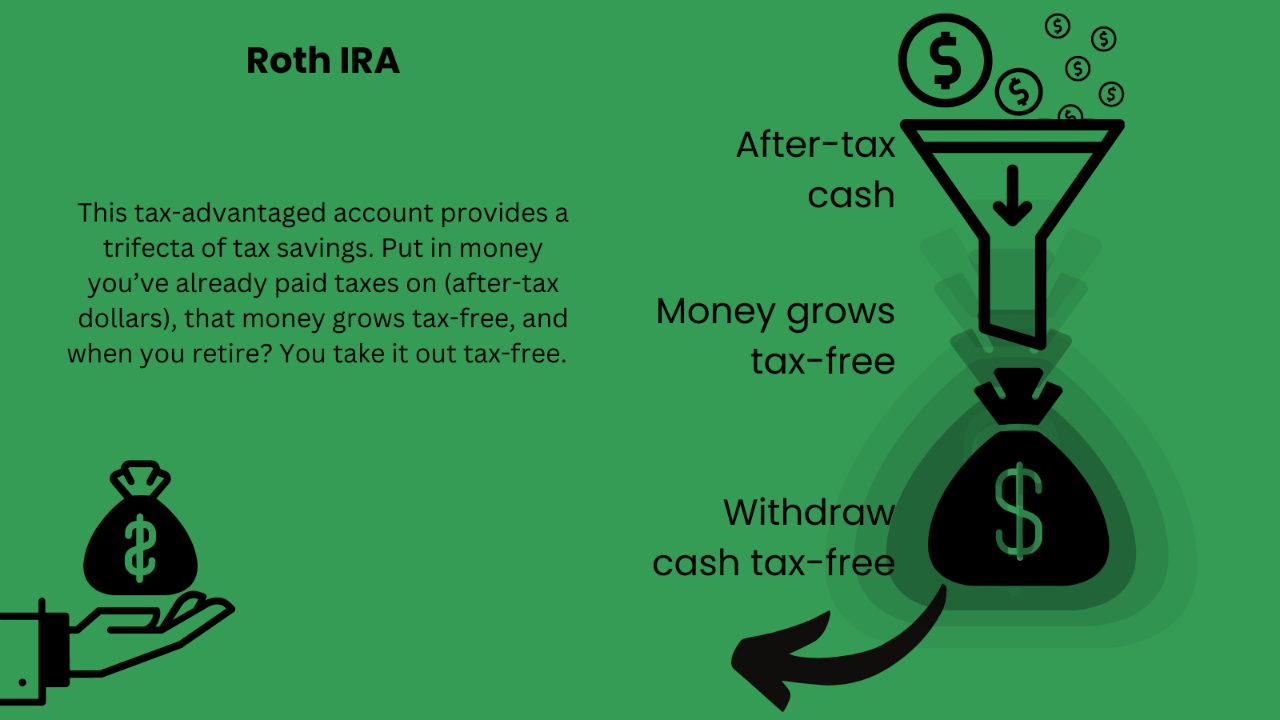

🧠 What’s a Roth IRA?

A Roth IRA is a special kind of retirement account where:

- You put in money you’ve already paid taxes on (after-tax dollars)

- That money grows tax-free

- And when you retire? You take it out tax-free

In other words, you’re taxing the seed, not the harvest. 🍎

💡 Why It’s a Power Move:

✅ No taxes on withdrawals after age 59½ (as long as it’s been 5 years)

✅ Withdraw contributions anytime, no taxes or penalties

✅ No required minimum distributions (RMDs)—unlike traditional IRAs or 401(k)s

✅ Perfect for tax-savvy investors who expect to be in a higher tax bracket later

💬 If you're in your 20s, 30s, or 40s without a Roth IRA... you're paying the tax man.

🚦Who Can Contribute in 2025?

You must be earning less than $150,000 (Based on your Modified Adjusted Gross Income (MAGI)) to fully contribute to your Roth IRA. Assuming you can, your max contribution for 2025 is $7,000 (or $8,000 if you’re 50+). Also, married couples filing jointly must earn less than $236,000 (MAGI).

🛠 How Do You Fund It?

- Regular contributions

- Spousal contributions

- Rollovers & conversions

- Transfers

Just remember: All contributions must be made in cash—no stocks or crypto directly.

📈 What Can You Invest In?

Roth IRAs can hold stocks, ETFs, mutual funds, bonds, and CDs.

Pro Tip: Your Roth IRA account works in a very similar way to your investment account. If you are a low-risk investor, it makes sense to maintain the same level of risk with your Roth IRA.

⚖️ Roth IRA vs. Traditional IRA

Pro Tip: If you think taxes are going UP (and let’s be real, they probably are), then a Roth IRA is probably your better option.

🧾 Withdrawals: When & How

- Qualified Withdrawals (after 59½ and 5 years): tax-free 💸

- Non-Qualified Withdrawals (early): may pay taxes + 10% penalty unless it’s for:

- First-time home ($10K limit)

- College expenses

- Un-reimbursed medical costs

- Childbirth/adoption ($5K)

Disability or death

FIFO rules apply—your contributions come out first.

❤️ The Spousal Roth IRA

If your spouse doesn’t earn income, you can contribute to a Roth IRA on their behalf. The same limits apply, but you can double your household’s tax-free retirement game.

🚀 Final Thoughts: Why You Need One Yesterday

If you’re young and just starting out—or even if you’re late to the game—Roth IRAs are a no-brainer for long-term wealth. Tax-free growth, flexible withdrawals, and no RMDs? Yes please.

🧠 Your future self doesn’t want a tax bomb in retirement.

👉 Action Steps:

- Open a Roth IRA (Fidelity, Vanguard, Wealthfront—pick your flavor)

- Automate contributions monthly (aim for $583.33/month if under 50)

- Invest wisely—keep fees low, stay diversified

- Leave it alone and let compound interest do its magic

"If you want tax-free income for life, the Roth IRA is your ticket. Don’t wait until you’re older to get smart."

✅ Check out my favorite Credit Cards

✅ Take advantage of my FREE Financial Freedom Faster eBook

This isn’t just saving. This is strategy.

- Steve

Disclaimer:

The following article is strictly the opinion of the author and is not to be considered financial/investment advice. CTL Community LLC and the author of this article do not claim to be a registered financial advisor (RIA) or financial advisor. Please visit our terms of service and privacy policy before reading this article. "Call to Leap may earn affiliate commissions from the links mentioned. Call to Leap is part of an affiliate network and receives compensation for sending traffic to partner sites such as ImpactRadius, CardRatings, MyBankTracker, and more."

Read more Curated Articles